US mortgage applications fell 9.7% over holiday-adjusted two-week span

MBA data showed lower loan application volume despite a decline in the average 30-year conforming mortgage rate to 6.25%.

By David L. Chen · Senior Columnist

· 3 min read

US mortgage application volume fell 9.7% over the two weeks ended January 2, 2026, even as the average 30-year conforming mortgage rate declined to 6.25%, according to the Mortgage Bankers Association. The figures point to a housing finance market still sensitive to rate moves, with refinancing elevated from a year earlier but purchase activity easing after the holidays.

The MBA said its Market Composite Index, which tracks mortgage loan application volume, declined 9.7% on a seasonally adjusted basis from two weeks earlier. The trade group said the latest survey results include a holiday adjustment, an important factor because application activity can be distorted around Christmas and New Year’s.

On an unadjusted basis, the composite index fell 28% compared with two weeks earlier, according to the MBA. Unadjusted measures do not strip out seasonal or calendar effects, so holiday periods can show larger swings than adjusted indexes.

Refinancing showed a sharper adjusted decline over the two-week period. The MBA’s holiday-adjusted Refinance Index decreased 14% from two weeks earlier, while the unadjusted index dropped 31%. Despite those declines, refinance demand remained well above year-earlier levels: the adjusted measure was 133% higher than the same week in 2025, and the unadjusted measure was up 108%.

Purchase applications also softened. The MBA said the seasonally adjusted Purchase Index declined 6% from two weeks earlier. On an unadjusted basis, purchase applications fell 23% over the same span but remained 10% higher than in the comparable week a year earlier.

Rates moved lower

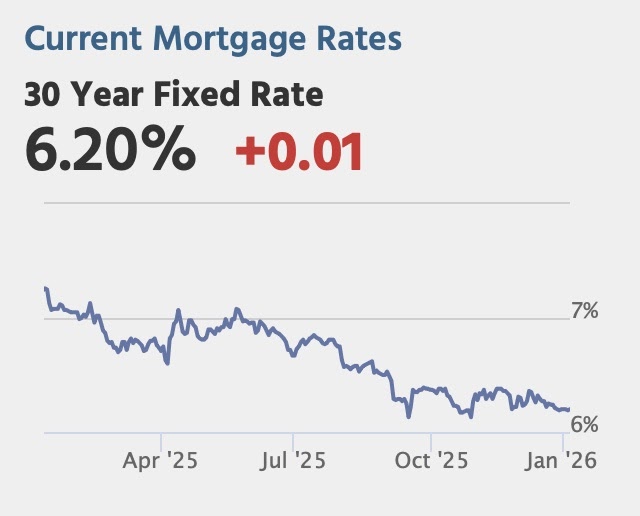

The average contract rate for 30-year fixed-rate mortgages with conforming balances of $806,500 or less fell to 6.25% from 6.32%, according to the MBA. Points, including the origination fee, decreased to 0.57 from 0.59 for loans with an 80% loan-to-value ratio.

A lower mortgage rate can reduce monthly payments for new borrowers and can make refinancing more attractive for homeowners whose existing loans carry higher rates. Refinancing demand, however, depends on the gap between a borrower’s current coupon and prevailing rates, as well as closing costs, credit standards and the borrower’s expected time in the home.

Joel Kan, the MBA’s vice president and deputy chief economist, said mortgage rates began the year at 6.25%, the lowest level since September 2024. He said refinance applications rose 7% for the week but were running at a slower pace than in the period before the holidays.

Kan also said Federal Housing Administration refinance applications increased 19%, describing the move as a partial recovery from a decline in the previous week. He said the MBA expects mortgage rates to remain near current levels, with refinancing opportunities emerging during weeks when rates fall.

Loan sizes declined

Kan said purchase applications were 10% above their year-earlier level but declined over the week as conventional and FHA applications fell. He said the average loan size was $408,700, the lowest in a year, reflecting lower average loan sizes across both conventional and government loan categories.

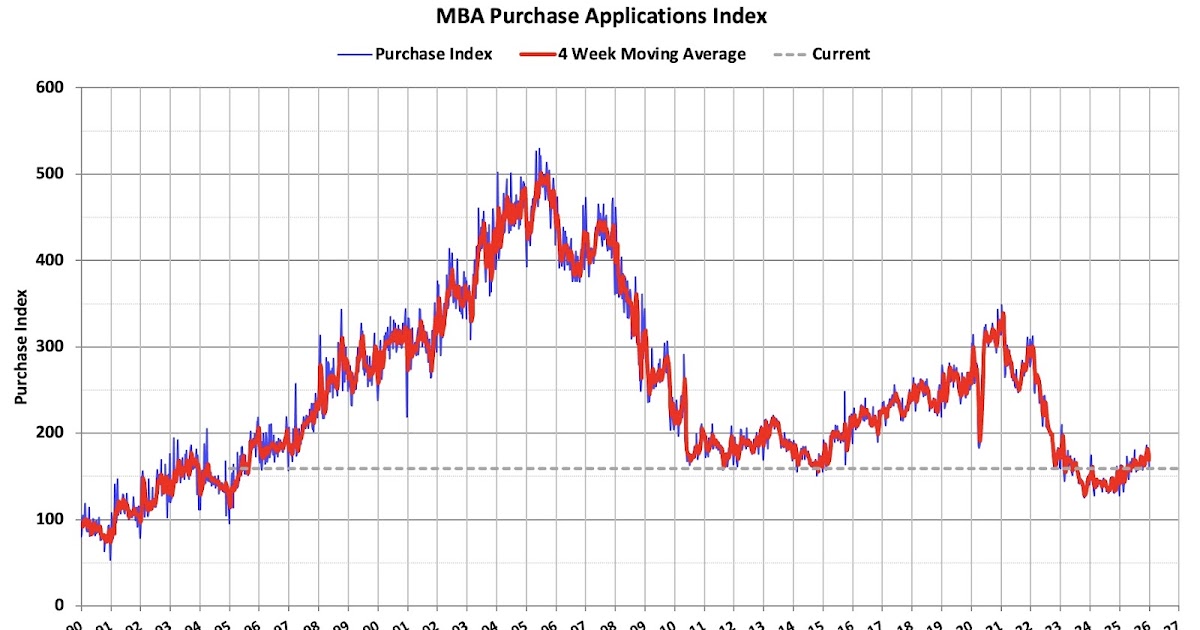

Calculated Risk, the finance and economics blog that published charts of the MBA data, said purchase application activity remains depressed, while standing above the lows reached in 2023 and above the weakest levels recorded during the housing bust. The blog also said the refinance index had risen from its bottom as mortgage rates declined, but had retreated from a recent September peak as rates moved sideways.

This story draws on original reporting from Calculated Risk.