US mortgage debt rose $108 billion in third quarter, Fed data show

Federal Reserve flow-of-funds data showed mortgage debt growth was flat from the prior quarter, according to Calculated Risk.

By Ingrid Halvorsen · Staff Writer

· 2 min read

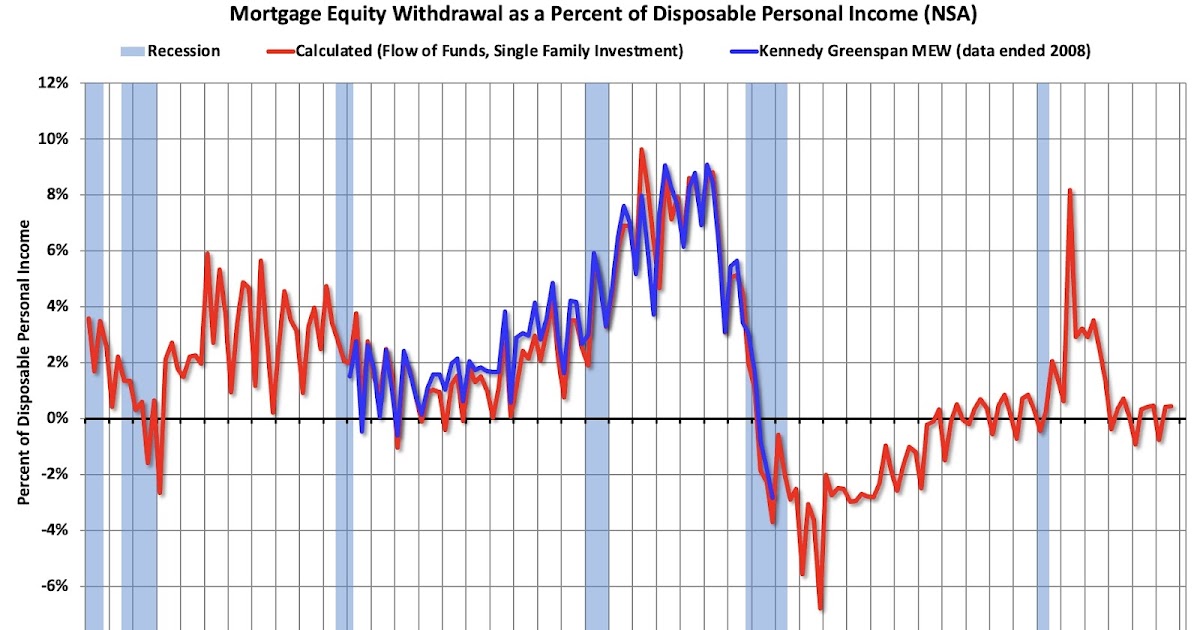

US mortgage debt increased by $108 billion in the third quarter of 2025, matching the second-quarter rise, according to Federal Reserve Financial Accounts data cited by Calculated Risk. The figures suggest mortgage borrowing continued, but Calculated Risk said the so-called home-equity “ATM” that marked the housing bubble remained mostly closed.

The Federal Reserve’s Financial Accounts of the United States, also known as the Z.1 or flow-of-funds report, track the liabilities and assets of households, businesses and other sectors. In housing, the mortgage-debt series is watched because it can capture both borrowing tied to home purchases and borrowing that extracts cash from existing home equity.

Calculated Risk said the mid-2000s housing bubble was accompanied by a large rise in mortgage debt as homeowners borrowed heavily against home values they believed had increased. That borrowing contributed to the later housing bust, according to Calculated Risk, because falling house prices left many borrowers with mortgages larger than the value of their homes.

Mortgage equity withdrawal works when a homeowner increases mortgage borrowing against an existing property, often through refinancing or other mortgage credit, and uses the proceeds outside the original home purchase. The aggregate mortgage-debt data do not isolate that activity on their own, because some new debt also finances the construction or purchase of new homes, which adds to the housing stock.

Calculated Risk emphasized that distinction in its reading of the third-quarter data. The $108 billion increase in mortgage debt cannot be treated entirely as equity withdrawal, because part of the borrowing is associated with buyers purchasing newly built homes.

The blog also noted a long post-crisis adjustment in household mortgage liabilities. After the housing bust, mortgage debt declined for almost seven years, according to Calculated Risk, as distressed sales including foreclosures and short sales eliminated a significant amount of debt.

The latest figures therefore sit between two different signals. On one side, mortgage debt is still rising in nominal terms. On the other, Calculated Risk’s interpretation is that the pattern does not resemble the bubble-era expansion in mortgage borrowing against home equity.

For policymakers and market participants, the distinction matters because mortgage debt growth can reflect different economic channels. Borrowing that funds new housing supply has different implications from borrowing that converts home equity into cash for other spending. The Federal Reserve data provide the balance-sheet totals, while the allocation between those uses requires further analysis beyond the headline mortgage-debt increase.

This story draws on original reporting from Calculated Risk.