US industrial output trails expectations as manufacturing stalls

Industrial production rose 0.1% month on month, below Bloomberg consensus, while manufacturing output was unchanged.

By David L. Chen · Senior Columnist

· 2 min read

US industrial production rose 0.1% month on month, short of the 0.2% gain expected in the Bloomberg consensus, according to Federal Reserve data and consensus figures cited by Econbrowser. Manufacturing production was flat, compared with expectations for a 0.1% increase.

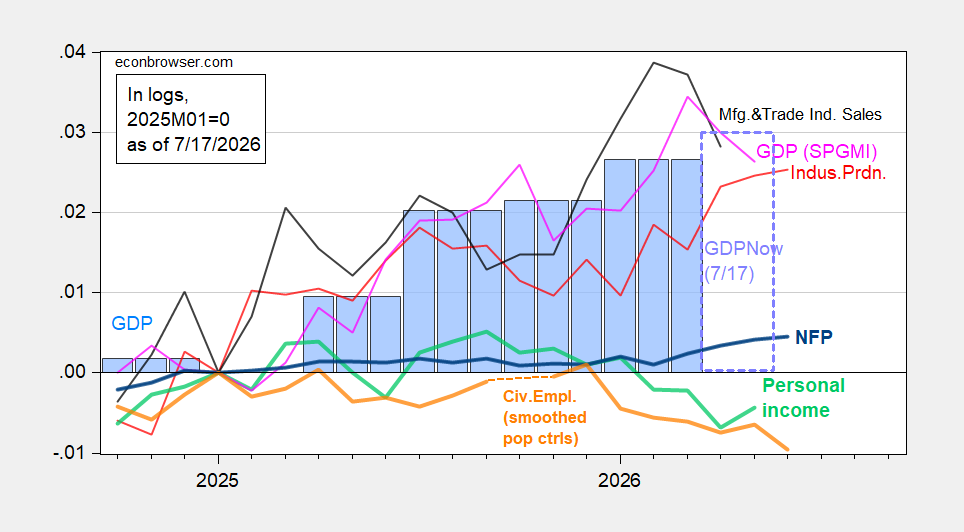

The production readings added a softer factory signal to a broader set of US business-cycle indicators. Econbrowser reported that the Atlanta Fed’s GDPNow estimate for first-quarter growth stood at 1.7% quarter on quarter at an annualized rate, below the New York Fed’s 2.7% nowcast and Goldman Sachs tracking at 2.4%.

Nowcasts are model-based estimates prepared before official GDP figures are published. They can diverge because each model uses a different structure for translating incoming monthly data into an estimate of quarterly output growth.

Broader indicator set

Econbrowser’s compilation placed industrial production alongside several measures used to assess the business cycle. The first chart included nonfarm payroll employment, civilian employment with smoothed population controls, industrial production, real personal income excluding current transfers, manufacturing and trade sales, monthly GDP and quarterly GDP.

The data cited for that comparison came from the Bureau of Labor Statistics via FRED, the BLS, the Federal Reserve, the Bureau of Economic Analysis 2026 first-quarter third release, and S&P Global Market Intelligence. Econbrowser said the series were shown in logs and normalized to January 2025.

A second comparison focused more closely on labor, factory activity, retail demand and transport. It included civilian employment adjusted to a nonfarm-payroll concept with smoothed population controls, manufacturing production, ADP private nonfarm payroll employment, CPI-deflated real retail sales, freight services indexes, a coincident index and gross domestic output.

Sources listed for that second set included the BLS, ADP via FRED, the Philadelphia Fed, the Bureau of Transportation Statistics, the Federal Reserve via FRED and the BEA’s 2026 first-quarter third release.

Econbrowser also noted that, in the pre-Covid period, GDPNow had been relatively accurate at the nowcast horizon cited, roughly two weeks before publication of the advance GDP release. The latest comparison nevertheless showed a spread of one percentage point between GDPNow and the New York Fed estimate, with Goldman Sachs tracking between the two.

This story draws on original reporting from Econbrowser.